Letztes Update: 13. January 2024

This article was written in collaboration with and with the support of Descartes Vorsorge. The content reflects my own opinion.

Life courses are rarely linear these days – mine is one big patchwork quilt – and suddenly, after a life event, you’re faced with the question of what to do with your saved pension fund money. This article deals with how such vested benefits are created and how they can best be parked or invested. Finally, I share my experience with the digital pension provider Descartes Finance, where I have a vested benefits account and a pillar 3a account, and show you the differences with other providers.

What are vested benefits?

First of all, the absolute basics: If you are affiliated with a pension fund through your employer, the employer pays the so-called BVG contributions. The BVG entry threshold, from which employees must be compulsorily insured in the occupational pension scheme, is CHF 21,510 in 2021. The employer pays part of the contributions, the other part is deducted from your salary. Together with the interest charged annually, this builds up your retirement assets. And this money is yours. If you change employer, your BVG retirement assets will also be transferred from the pension fund of your old employer to the pension fund of your new employer.

Now, however, you may be laid off and not be able to find a new job immediately afterwards. Or you go on a longer trip, dedicate yourself full-time to the offspring or start your own business. For all of these events, you must also leave the employer’s pension fund when you leave the employer. Your pension assets now become vested benefits and you can choose to which vested benefits institution they should be transferred.

Incidentally, if you don’t tell the old pension fund where to transfer the money, it will park it in a vested benefits account at the Stiftung Auffangeinrichtung BVG after two years at the latest.

What to do with vested benefits?

For vested benefits, the word “park” has become accepted. Well, depending on the parking space, there is a parking meter, the car rusts away and loses value. That would be the account solution. Some banks have now introduced a monthly account maintenance fee for vested accounts and offer only measly interest rates.

| Bank | Interest rate | Account maintenance fee |

| Credit Suisse | 0.01% | CHF 9 per quarter |

| Migros Bank | 0.01% | |

| PostFinance | 0.01% | CHF 9 per quarter |

| Raiffeisen | 0.01% | |

| UBS | 0.01% | CHF 3 per month |

| ZKB | 0.1% |

I prefer the word “invest”, which brings us to a vested benefits deposit. As with pillar 3a, you can invest your vested benefits profitably in securities. In the long term, you have a higher chance of a return than with the account solution.

Now it depends a bit on how long your investment horizon is. If you’re only going on a world trip for five months, the account solution is probably still the right choice because of the fluctuations in the stock market. If you plan to take a break of three to five years, you could look at a securities solution with a similar equity component as the pension funds. By the way, on average, the share of equities in pension funds is about 33%. And if your investment horizon is longer, then you could choose the highest equity allocation, depending on your risk appetite.

Note: As soon as you have a new employer and are affiliated with a pension fund through this employer, you must transfer your vested benefits to the new pension fund. Small chamber: This is mostly not controlled.

To minimize the cluster risk of only one provider, it is possible to split vested benefits. You can therefore instruct your previous pension plan to transfer your vested benefits to a maximum of two vested benefit institutions. However, subsequent splitting is not possible.

Choosing two independent providers is highly recommended. Not only do you minimize cluster risk, but you can run two different strategies and save on taxes when you draw.

Descartes precaution

Now we finally come to the provider Descartes Vorsorge. You already know this from the pillar 3a comparison.

Descartes Finance launched its robo-advisor for free assets in 2016, making professional asset management accessible to private investors. The minimum deposit at the owner-managed start-up is currently CHF 25,000, but is to be significantly reduced in the near future. The following three investment strategies are available in free assets:

- Descartes Index Responsible (Swisscanto index fund)

- Descartes Minimum Risk ESG (Fund of OLZ)

- Descartes Focus Sustainable (fund of Swisscanto Invest)

Since 2019, Descartes Finance has also been offering digital investment solutions for tied pension provision with Descartes Vorsorge.

In the meantime, Descartes has been able to win over various wealth advisors who use Descartes’ digital solutions in both free and tied pension provision. For example, Glarner Regionalbank offers its customers Descartes’ pension solutions.

Descartes is the only Swiss provider that is completely independent of banks and products. The funds used come from an owner-managed fund manager and are also available to other providers; the foundation and the custodian bank are also independent.

Descartes investment strategies

There are a total of four investment strategies to choose from, which differ according to the risk level and the share of equities:

- Low (20%)

- Moderate (40%)

- Medium (60%)

- High (80%)

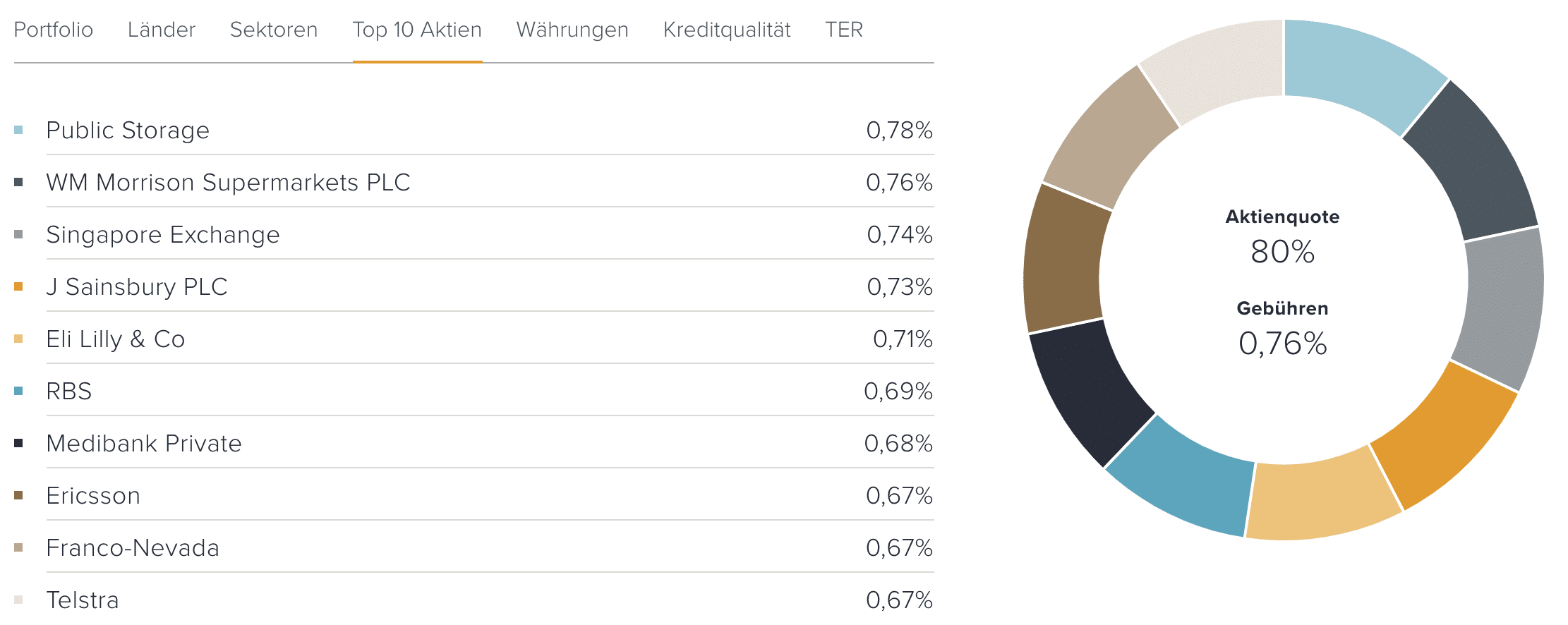

Below the respective risk level, you can see transparently on the website how your portfolio is structured, which countries are represented with which percentages.

And this is where the first difference to other providers is noticeable: The weighting of the regions. For example, the USA is represented in the “High” strategy with only 13%, and Switzerland with 12%. Other providers weight Switzerland at over 70%, for example. Thus, individual shares are sometimes represented with more than 7% – for example Nestlé. Not so with Descartes precaution. The largest share accounts for just 0.78%. At the moment, this is Public Storage. The fact that you’ve probably never heard of this American self-storage provider is quite possible.

Minimum variance

So how does Descartes come up with this enterprise? Descartes does not manage the funds itself, but uses OLZ’s funds. OLZ is a Bern-based asset manager in the field of sustainable and risk-based portfolio optimization and one of the largest Swiss asset managers. The “secret” behind the greatest weight of public storage is behind the word “risk-based.” Indeed, OLZ constructs portfolios according to the concept of “minimum variance,” also known as “minimum volatility.”

Explained very briefly: Shares are known to fluctuate. This is called volatility and this deviation from the mean can be measured. The goal of a minimum variance portfolio is now to select those stocks that reduce the volatility of the overall portfolio and thus the overall risk of the portfolio.

As a result, OLZ funds slump less in a crash and rise less in stock market bull markets. This means that you can hold a higher proportion of equities for the same level of risk.

In summary, Descartes takes a more active approach than its competitors, which has a positive effect on diversification. Pension funds also invest actively in Swiss equities in particular, because the three largest companies would otherwise take up a very large share of the portfolio.

You don’t have vested funds to invest? Descartes Vorsorge also offers the same investment strategies for pillar 3a. There, with the strategy “Very high” even 100% shares are possible.

Descartes sustainability

Descartes invests exclusively ESG-compliant in all strategies and was thus the pioneer among the young digital providers. Companies that violate fundamental sustainability criteria are screened out. Thus, companies that operate mainly in the following areas are excluded:

- Weapons

- Gambling

- Pornography

- Tobacco, Alcohol

- Coal

- Nuclear power

- Genetic engineering

At the beginning of 2022, Descartes adjusted its investment strategy to focus even more consistently on sustainability. Companies with lower CO2 emissions are now weighted more heavily than companies that have a greater impact on the climate. As a result, the CO2footprint of the new investment strategy is at least 30 percent lower than that of the market index.

But it is not only at the portfolio level that Descartes focuses on sustainability. For example, Descartes’ software was developed in Switzerland and hosting is also done in Switzerland by a Swiss company. A look at the photos of the board of directors also reveals that it is diverse and does not consist of older, white-haired men. Further exciting projects in the area of sustainability are being planned.

Descartes registration and consultation

With the 2nd Pillar Calculator on the Descartes Vorsorge website, you can calculate your retirement capital yourself and run through the four investment strategies. When you decide to open a securities account with Descartes, you first enter your personal information and after answering ten questions, an investment profile tailored to you will be proposed. If you agree, you can simply sign the advance care directive digitally. After five minutes, everything is done.

However, if you are unsure which investment strategy is the most suitable for you and you want to have the splitting explained again or you have another question, you can contact the Descartes team for a personal consultation. You can reach it by email and phone or you can book a no-obligation pension consultation on the website.

On the website of Descartes Vorsorge you will also find an informative blog . The new blog format “Women and Finance” is intended to motivate people to take a self-determined approach to finances.

Descartes all-in fees

The total annual fees in the vested benefits area are – depending on the equity quota – between 0.65% and 0.76% and consist of the custody costs (custody and foundation fees; 0.20%) and the product costs (TER; 0.45 to 0.60%). The product cost already includes the Descartes fee of 0.20%. The fees are deducted on a quarterly basis.

Due to the more active approach, Descartes Vorsorge’s fees are slightly higher than the other digital providers. If, on the other hand, they are compared with the banks, they are still around 50% lower.

There are no additional costs for opening or balancing the account. In addition, the funds are bought for you in Swiss francs. Foreign currency fees are therefore also not incurred. You can find a blog post on yield-diminishing foreign currency fees here. When you buy funds from some dinosaurs, you’re charged what’s called an issuance commission, and when you redeem, you’re charged a redemption commission. This can amount to as much as 5%. Descartes can do without at all. More details about Descartes’ fees including a calculation example can be found here.

Descartes cockpit

On the basis of my personal Descartes Vorsorge vested benefits portfolio, we lastly take a look at the cockpit. Access is via web app. A smartphone app is not available. As long as a website is responsive, I don’t think it needs an app – especially for long-term investing. What do I want to check my assets every day if I’m not going to access them for thirty years anyway?

To log in to your Descartes Pension Vested Benefits Deposit, enter your username and password and you will receive a code via SMS.

The interface is very tidy and clear. At the top you see the total performance and the total assets. Further down, you can display either your Pillar 3a custody account or your vested benefits custody account. Here you can also find a chart that shows you the money-weighted return. You can find a blog post explaining the different types of returns here.

Under “Asset structure” you can see which fund has performed how. If you want more information about the funds, click on the ISIN and a PDF of the factsheet will open.

Under “My mailbox” you will find all contracts and regulations. The bank documents are also stored there. This way you can always track which funds were bought or sold and see transparently how many fees were deducted.

FAQ Free movement

Descartes all-in fees range from 0.65% to 0.76%.

No, you can only transfer 2nd pillar funds that are already tied up to a vested benefits account or custody account.

Yes, you can. However, only during the first twelve months after confirmation of self-employment by the AHV compensation fund.

Other reasons for reference include:

– Reaching the AHV retirement age (possible 5 years earlier)

– Home ownership promotion

– Purchase into the pension fund

– Leaving Switzerland

– Disability or death

Yes, it is possible. However, there are costs associated with certain providers. So it is best to inform yourself before the transfer.

No, there are no property, income or withholding taxes. The vested pension assets are not taxed until they are withdrawn.

Transparency and disclaimer

This article was written in collaboration with and with the support of Descartes Vorsorge. The content reflects my own opinion. More about transparency and paid contributions can be found here.

If you open accounts or business relationships, order products or services through my links and codes, I may receive a commission for doing so. However, you will not suffer any disadvantages such as higher prices or the like. The terms and conditions of the respective providers apply. Affiliate links are marked with a *.

Investments are associated with risks which, in the worst case, can lead to the loss of the capital invested.

All publications, i.e. reports, presentations, notices as well as contributions to blogs on this website (“Publications”) are for information purposes only and do not constitute a trading recommendation with regard to the purchase or sale of securities. The publications merely reflect my opinion. Despite careful research, I do not guarantee the accuracy, completeness and timeliness of the information contained in the publications.