Letztes Update: 28. September 2023

I was on vacation the other day – that’s why it was a bit quieter here – and bought chewing gum. What does this have to do with a financial blog? I bought the gum abroad with five different cards to compare the foreign currency rates of the neo-banks.

First finding: French self-service checkouts are much more closely monitored than in Switzerland (if you buy five packs of chewing gum with different cards, you attract attention), and the second finding: the differences are quite large. But let’s take it one step at a time.

There are two ways a bank can make money when paying in another currency: On the one hand, it can fix the foreign currency rate. For example, define at what rate it sells you euros and at what rate it buys euros from you. And on the other hand, it may charge a handling fee on foreign currency transactions. Let’s take a closer look at the two options.

Foreign currency rates

So, there is the so-called interbank rate, the “real” rate, and on this the bank calculates a margin and then publishes its rates. The exact amount of this margin is usually not published by the bank. You just get an exchange rate displayed. To find out whether it is good or bad, you have to compare it with the “real” exchange rate.

The comparison service moneyland.ch wrote a study on this in 2018. The mean value of the foreign exchange rates at that time was a spread of 2.92%. If you would exchange your Swiss Francs into Euros and immediately back into Swiss Francs, the bank would have earned 2.92% on you. If you buy Euro and do not change back, then only half, that is 1.46%.

Incidentally, the markups are still lowest for the euro currency. The more exotic the currency, the higher the markups.

Processing surcharges

Some banks also call these surcharges “foreign currency or foreign transaction fee”, “foreign surcharges” or something similar. These are in addition to the bank’s own foreign currency rates!

The following processing surcharges are levied by the largest Swiss banks on credit card transactions abroad:

| Anbieter | Kreditkarte | Zuschlag/Gebühr |

| Credit Suisse | Bonviva World Mastercard Standard | 2.5% |

| Migros Bank | Kreditkarte Visa Free CHF (Viseca) | 1.5% |

| PostFinance | Mastercard Standard | 1.2% |

| Raiffeisen | Mastercard Silber | 1.75% |

| Swisscard AECS | Cashback Cards World Mastercard | 2.5% |

| UBS | Mastercard (Classic) | 1.75% |

| ZKB | Standard-Kreditkarte (Mastercard) | 1.7% |

Own research on the websites of the providers from September 1, 2021.

Small side note: Dear banks, if you publish prices of your services on the Internet, that’s nice. I lose patience with a multi-page PDF where the tables span two pages. Your print brochures may be nicely done, but just put them in the store and don’t use the Internet as a repository for PDFs.

Paying in foreign currencies with neo-banks

Since the emergence of neo-banks, processing surcharges began to slide or were even abolished altogether. The British app bank Revolut was the first major player to offer attractive exchange rates for Swiss citizens. In January 2020, the Swiss neo-bank neon followed suit, abolishing foreign surcharges and introducing attractive exchange rates. Since then, the big banks have been forced into action. For example, Credit Suisse has launched the digital banking offering CSX digital banking service and no longer charges processing fees.

Processing surcharges are easy to compare, but what about exchange rates? And that brings us back to chewing gum. I bought them all in the same store, on a weekday right after each other. In the table below I have listed the exchange rates finally recorded.

Some neo-banks also charge a processing surcharge in addition to the foreign currency rate. This is included in the exchange rate surcharge and marked accordingly.

| Anbieter | Wechselkursaufschlag |

| neon | 0.01% |

| Revolut | 0.06%* |

| Wise | 0.4%** |

| YAPEAL | 0.19% |

| Yuh | 1.27%*** |

* on weekends and above a certain exemption limit additional surcharges/fees apply

** incl. Fee from 0.39%

*** incl. Fee from 0.95%

Graphically it looks like this:

I actually wanted to do the “experiment” a second time on another day, but my French, like the English of the first self-service checkout supervisor, needs a lot of improvement. That’s why I limited myself to two purchases this time.

Because the “real” exchange rate is a bit more difficult at the weekend, I have chosen the daily maximum exchange rate as a comparison exchange rate here.

| Anbieter | Wechselkursaufschlag |

| CSX | 2.19% |

| neon | 0.31% |

What do I care about all the decimal places?

For a pack of chewing gum of EUR 1.15, the difference may be negligible. But extrapolated over the entire vacation, the decimal places do make a difference.

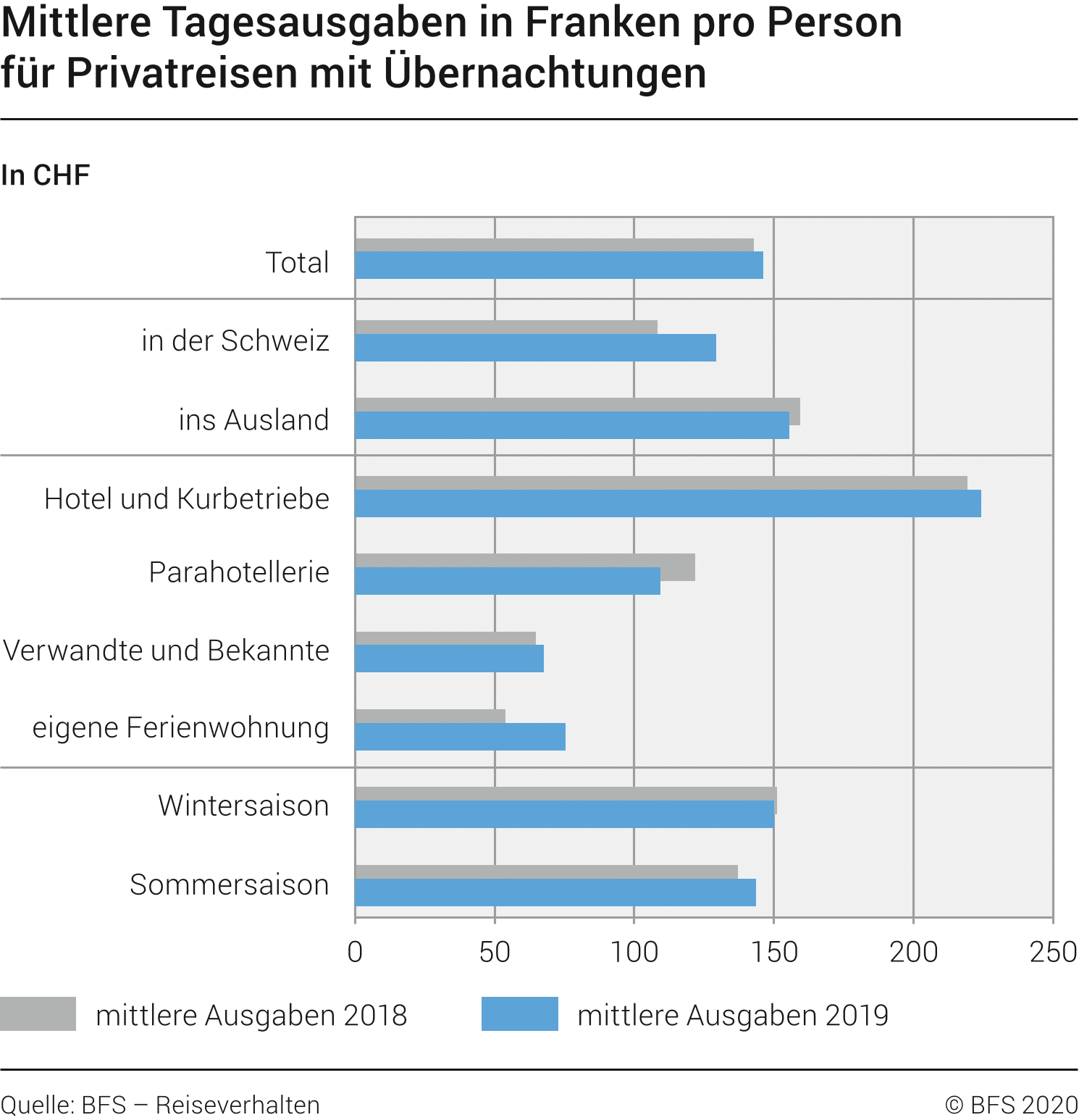

According to the Swiss Federal Statistical Office (SFSO), the average daily expenditure per person on vacations abroad is CHF 156. This includes expenses for transportation, lodging, meals, and other costs incurred during a trip.

If we calculate with two weeks of vacation for two persons, we come to a sum of CHF 4’368.

If you were to pay for the entire vacation with neon, you would have to cede a paltry CHF 0.44 to neon with the 0.01% surcharge in our example above (CHF 13.54 in the example below with the 0.31% surcharge).

And as a counterexample, we calculate with a classic credit card and the surcharge on foreign currency rates determined by moneyland of 1.46% plus a processing surcharge of 1.85%. This results in a total of 3.31% and an amount of CHF 144.58 – with this you can go out for a nice meal for two.

Concluding remarks

The exchange rates I calculated are a snapshot, i.e. a single sample. On another day, with another currency, the result could be different, as you can see in the second table. Some banks convert immediately, some with a rate set once a day, or similar. Sometimes you therefore get a better course, sometimes a worse one.

Advertising

Transparency and disclaimer

I was not paid by anyone for this blog post, it reflects my subjective opinion.

If you open accounts or business relationships, order products or services through my links and codes, I may receive a commission for doing so. However, you will not suffer any disadvantages such as higher prices or the like. The terms and conditions of the respective providers apply. Affiliate links are marked with a *.

Investments are associated with risks which, in the worst case, can lead to the loss of the capital invested.

All publications, i.e. reports, presentations, notices as well as contributions to blogs on this website (“Publications”) are for information purposes only and do not constitute a trading recommendation with regard to the purchase or sale of securities. The publications merely reflect my opinion. Despite careful research, I do not guarantee the accuracy, completeness and timeliness of the information contained in the publications.